Commercial mortgages suffer while home & auto loans "thrive"...

Today’s charts and analysis are kindly provided by my friend Will Carpenter. Will has been doing research on asset-backed securities in Covid since this summer. Please enjoy:

For anyone that might be wondering about how the pandemic has hit bigger businesses, the commercial mortgage space tells a very polarizing story that is still ongoing. These mortgages are essentially large loans made to business entities like malls, hotel chains, office buildings, etc. Then they can be packed into CMBS (commercial mortgage-backed securities) that are essentially the same concept as the mortgage-backed securities that created problems in 2008.

Thanks to our friends at the SEC, a good deal of CMBS security performance is available on a monthly basis and tells a decent bit about which property sectors have been the hardest hit by COVID and are struggling to pay up.

The figure below illustrates 30+ delinquencies in mortgage loans for about 6,000 properties country-wide. The notable spikes being within lodging, retail, and mixed use properties. Lodging alone has been hovering around 25% since April (!) In other words, 25%+ businesses haven’t paid back their loans for 30+ days (90 days would be the subjective threshold for essentially defaulting). The situation is not showing substantial signs of a “V-shaped" recovery.

This is very different from some other debt industries that have had much less trouble, such as consumer mortgages and auto loans. Both these areas have received more direct help by way of loan forbearance and government stimulus. In fact, there have been actually significantly more mortgage originations for higher credit scores over the past year compared to previous years. In other words, because the interest rate is so low, it's very attractive for decently well-off people to swoop into the home mortgage market. Big difference from the commercial mortgage market, which has proven far more cumbersome and difficult to provide forbearance to.

In fact, betting on the consumer mortgages seems to have paid off thus far for many investors focused on popular consumer debt like home, auto, and credit card loans. Compared to the commercial mortgage market, they're "thriving!"

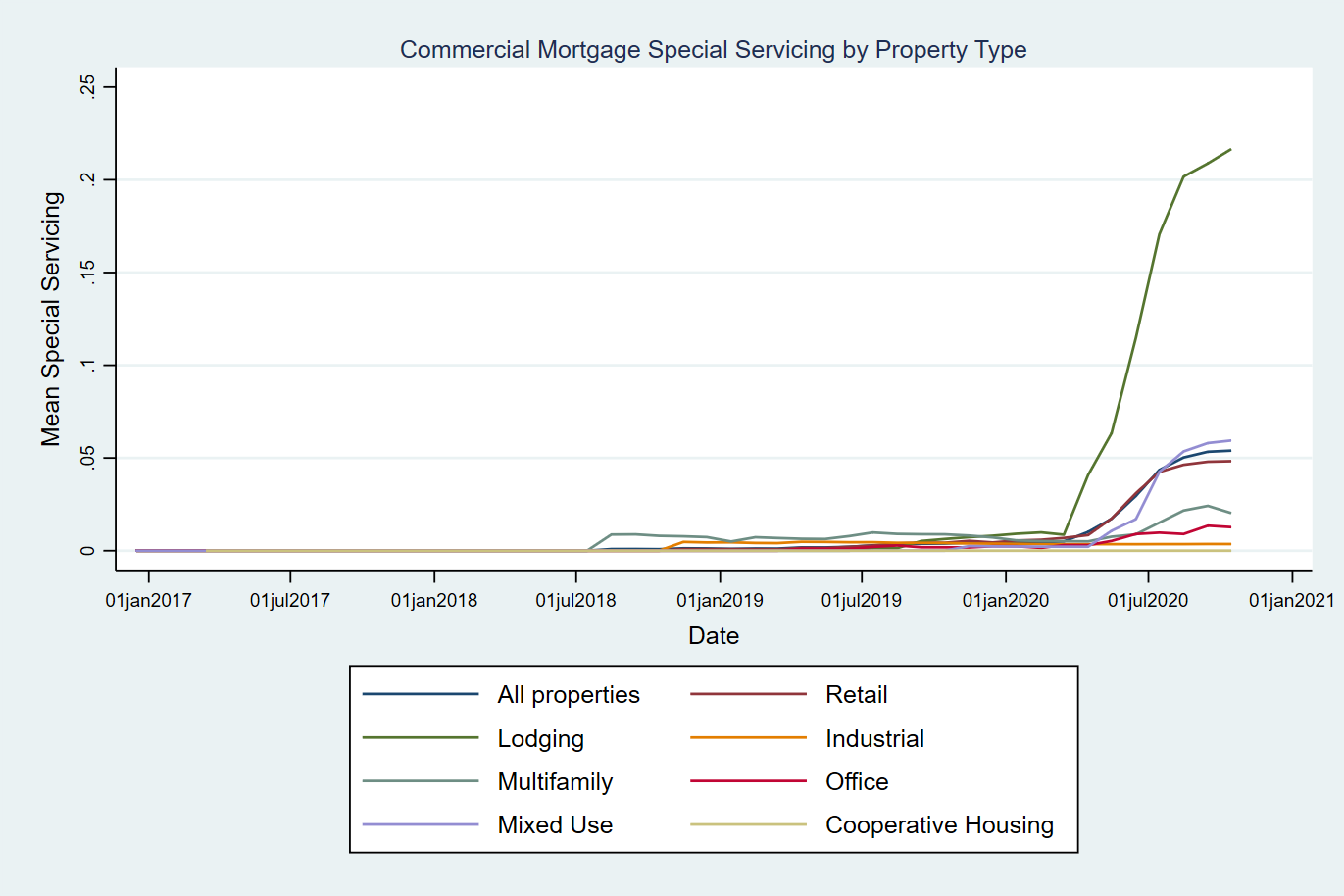

At this point, it could be worth it to keep on eye on office space (red line) as an industry with a "lagged fate" as the notions of returning to work seem to be less certain for many large corporations. On the other hand, properties like industrial space or cooperative housing have been virtually unaffected....extremely polarizing trends we are still seeing.

Evidently, these levels of distress are unprecedented over the past few years and are only comparable to around 2012 when the sector was still suffering from the Great Recession. The situation could also get worse as commercial property prices, especially in cities, have been dropping.

In addition to delinquency levels, we can also examine a close cousin of delinquency: special servicing. Loans that are put into special servicing within CMBS are essentially signalling that they are in distress and likely to default in the near future. The figure below illustrates levels for special servicing by month and property type. Clearly, these trends show almost no sign of dropping within any property type. Again, it's fairly clear that lodging, retail, and multi-use are suffering the most here.

This is just another dimension of the pandemic worth considering and could be relevant if you're considering any real estate investment trusts (REIT) to buy or if you might be simply wondering if what types of businesses could be out of the woods.

This is also just data I organize for research so feel free to reach out to me with any questions. It can be sliced and diced many different ways if you could be interested in learning more about geographics or other property types not included here (these are the major ones).

Another great source of information on commercial mortgages is Trepp that is a big name for monitoring CMBS if you would like to read more on the topic.

You may reach Will at wrc4@princeton.edu.